India and the US are a signature away from reshaping Asian sourcing

12 May 20265 min read

Summary

- US Deputy Secretary of State Christopher Landau confirmed on 6 May that a bilateral trade agreement between Washington and New Delhi is very close to finalisation, with one outstanding issue remaining.

- The framework agreed in February 2026 would cut US tariffs on Indian goods from 25 to 18 per cent; India has separately committed to purchasing US$500 billion in American goods over five years, according to the White House Joint Statement published in February 2026.

- For manufacturers building a China+n sourcing strategy (diversifying production across multiple countries rather than consolidating it in a single alternative to China), a finalised India-US deal changes the investment calculus in electronics, pharmaceuticals and textiles.

US Deputy Secretary of State Christopher Landau confirmed on 6 May that a bilateral trade agreement between the United States and India is very close to finalisation, with a single outstanding issue remaining before the deal can be signed. The framework agreed in February 2026 would cut the US reciprocal tariff on Indian goods from 25 to 18 per cent, with the 18 per cent rate taking effect immediately under Executive Order 14257 at the time of announcement, according to the White House Joint Statement published on 13 February 2026. India has separately committed to purchasing US$500 billion in American goods over five years. That figure is a procurement commitment by India, not a target for total bilateral trade volume.

The India-US trade negotiation has been in motion for several years but accelerated after the 2025 tariff escalation pushed manufacturers to speed up their China+n planning. China+n describes the shift from seeking a single alternative to Chinese manufacturing towards diversifying production across multiple countries simultaneously, spreading concentration risk rather than simply relocating it. India’s appeal as one node in that diversified structure has always been structural: a large domestic market, an English-speaking technical workforce and established pharmaceutical and textile export industries. What has been missing is the tariff certainty that makes a long-term sourcing commitment worth the capital expenditure.

A finalised deal would address that gap directly. At 18 per cent, US tariffs on Indian goods would be materially lower than the current 25 per cent and, for many product categories, lower than the tariffs applied to Chinese and Vietnamese goods. The differential creates a cost advantage that, for some manufacturers, is enough to justify moving production. India’s container manufacturing capacity, covered in an earlier VCA analysis of the country’s logistics expansion, is already growing in anticipation of this shift.

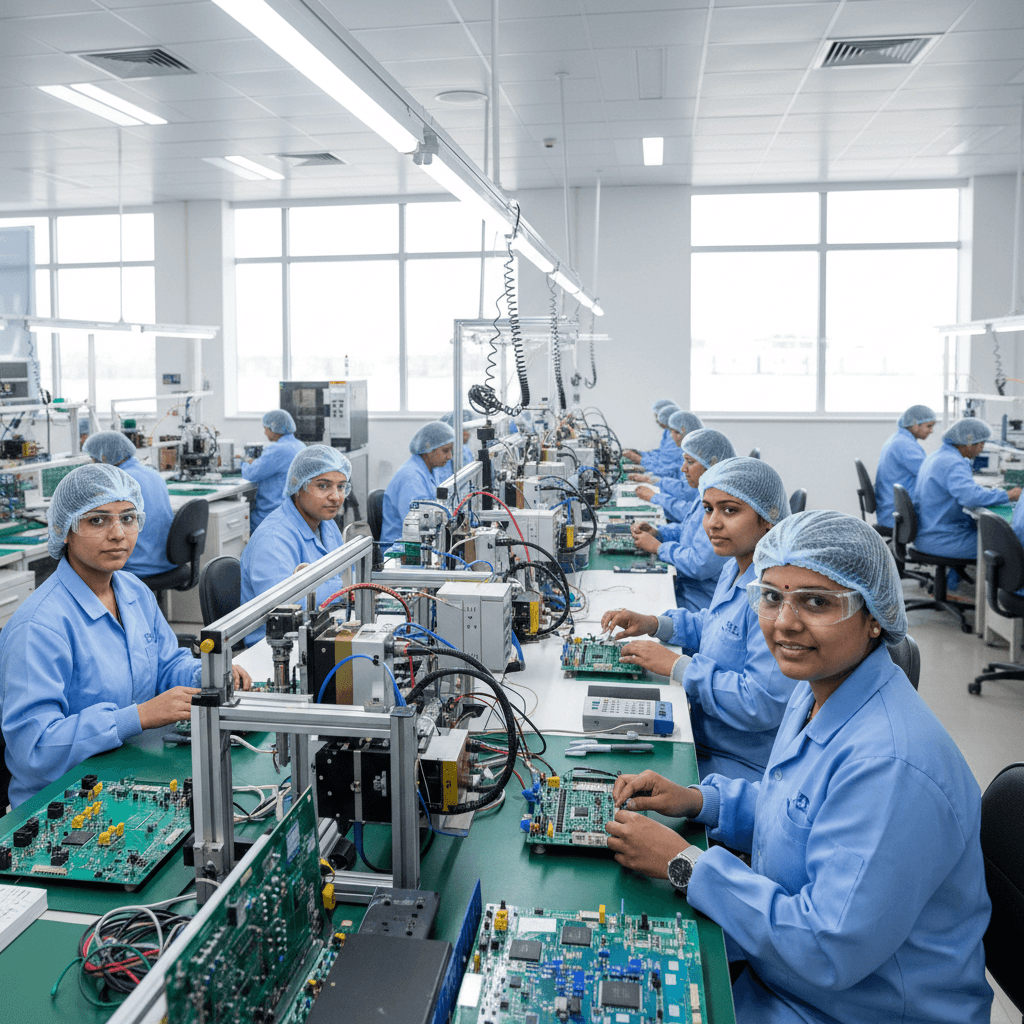

Electronics is the sector to watch most closely. India’s Production Linked Incentive scheme has attracted Apple, Foxconn and Samsung to expand Indian manufacturing, but the scale of that expansion has been constrained by uncertainty over export economics. A tariff reduction from 25 to 18 per cent changes those economics. Apple already assembles iPhones in Tamil Nadu and Karnataka, and a confirmed tariff advantage accelerates the investment case for expanding that capacity further.

Pharmaceuticals present a different dynamic. India is already the world’s largest supplier of generic medicines to the United States, supplying approximately 47 per cent of American generic prescriptions, according to US Food and Drug Administration import data cited by the India Brand Equity Foundation. A finalised trade deal does not fundamentally alter this supply relationship but it strengthens India’s position relative to other potential sourcing markets and reduces the political risk premium that large pharmaceutical buyers currently price into their Indian contracts.

The outstanding hurdle has not been publicly described by either side. Landau acknowledged on 6 May that he lacked specific information on when the deal would be signed, though he reiterated confidence that it was imminent. Agricultural market access and digital trade provisions are the areas where India has historically been most reluctant to concede ground in negotiations, making them the probable sticking points. Landau’s use of the phrase “very, very close” is notably more precise than the diplomatic language used in earlier rounds, suggesting the remaining gap is a defined issue rather than a structural impasse.

The deal is expected to be formally signed before the end of June 2026. Because the 18 per cent tariff rate has already been applied under executive order since February, a finalised agreement does not change the landed-cost calculation today. What it changes is the risk premium. An executive order can be reversed; a signed trade agreement carries political and legal costs to unwind. For supply chain planners, the signal is that the tariff rate is becoming durable rather than provisional. The relevant question shifts to which product categories benefit most and how quickly suppliers in those sectors can scale Indian production.

India’s limitations as a manufacturing destination deserve the same scrutiny as its opportunities. The country’s semiconductor and advanced electronics manufacturing base remains early-stage; the gaps that make China irreplaceable in high-complexity assembly do not disappear because a tariff agreement exists. State-level variation in industrial land acquisition, labour law and customs administration creates significant execution friction that does not appear in national-level investment promotion. Companies that treat India as a homogeneous market comparable in operational complexity to China after two decades of supply chain development will face surprises. The deal improves the economics. It does not resolve the execution risk.

The risk of waiting is asymmetric. Manufacturers who commit sourcing agreements to India in 2026 will benefit from lower landed costs as the tariff reduction takes hold, while competitors who wait will compete for supplier relationships and factory capacity that is no longer available at current rates. India’s contract manufacturing base, like China’s before it scaled, rewards early commitment over opportunistic late entry.

Manufacturers who have been treating India as a hedge against China dependence will need to decide, soon, whether the tariff trajectory makes it a primary destination rather than a contingency.

The India-US trade negotiation has been in motion for several years but accelerated after the 2025 tariff escalation pushed manufacturers to speed up their China+n planning. China+n describes the shift from seeking a single alternative to Chinese manufacturing towards diversifying production across multiple countries simultaneously, spreading concentration risk rather than simply relocating it. India’s appeal as one node in that diversified structure has always been structural: a large domestic market, an English-speaking technical workforce and established pharmaceutical and textile export industries. What has been missing is the tariff certainty that makes a long-term sourcing commitment worth the capital expenditure.

A finalised deal would address that gap directly. At 18 per cent, US tariffs on Indian goods would be materially lower than the current 25 per cent and, for many product categories, lower than the tariffs applied to Chinese and Vietnamese goods. The differential creates a cost advantage that, for some manufacturers, is enough to justify moving production. India’s container manufacturing capacity, covered in an earlier VCA analysis of the country’s logistics expansion, is already growing in anticipation of this shift.

Electronics is the sector to watch most closely. India’s Production Linked Incentive scheme has attracted Apple, Foxconn and Samsung to expand Indian manufacturing, but the scale of that expansion has been constrained by uncertainty over export economics. A tariff reduction from 25 to 18 per cent changes those economics. Apple already assembles iPhones in Tamil Nadu and Karnataka, and a confirmed tariff advantage accelerates the investment case for expanding that capacity further.

Pharmaceuticals present a different dynamic. India is already the world’s largest supplier of generic medicines to the United States, supplying approximately 47 per cent of American generic prescriptions, according to US Food and Drug Administration import data cited by the India Brand Equity Foundation. A finalised trade deal does not fundamentally alter this supply relationship but it strengthens India’s position relative to other potential sourcing markets and reduces the political risk premium that large pharmaceutical buyers currently price into their Indian contracts.

The outstanding hurdle has not been publicly described by either side. Landau acknowledged on 6 May that he lacked specific information on when the deal would be signed, though he reiterated confidence that it was imminent. Agricultural market access and digital trade provisions are the areas where India has historically been most reluctant to concede ground in negotiations, making them the probable sticking points. Landau’s use of the phrase “very, very close” is notably more precise than the diplomatic language used in earlier rounds, suggesting the remaining gap is a defined issue rather than a structural impasse.

The deal is expected to be formally signed before the end of June 2026. Because the 18 per cent tariff rate has already been applied under executive order since February, a finalised agreement does not change the landed-cost calculation today. What it changes is the risk premium. An executive order can be reversed; a signed trade agreement carries political and legal costs to unwind. For supply chain planners, the signal is that the tariff rate is becoming durable rather than provisional. The relevant question shifts to which product categories benefit most and how quickly suppliers in those sectors can scale Indian production.

India’s limitations as a manufacturing destination deserve the same scrutiny as its opportunities. The country’s semiconductor and advanced electronics manufacturing base remains early-stage; the gaps that make China irreplaceable in high-complexity assembly do not disappear because a tariff agreement exists. State-level variation in industrial land acquisition, labour law and customs administration creates significant execution friction that does not appear in national-level investment promotion. Companies that treat India as a homogeneous market comparable in operational complexity to China after two decades of supply chain development will face surprises. The deal improves the economics. It does not resolve the execution risk.

The risk of waiting is asymmetric. Manufacturers who commit sourcing agreements to India in 2026 will benefit from lower landed costs as the tariff reduction takes hold, while competitors who wait will compete for supplier relationships and factory capacity that is no longer available at current rates. India’s contract manufacturing base, like China’s before it scaled, rewards early commitment over opportunistic late entry.

Manufacturers who have been treating India as a hedge against China dependence will need to decide, soon, whether the tariff trajectory makes it a primary destination rather than a contingency.